By: HT Auto Desk | Updated on: 04 Apr 2024, 11:33 AM

The Air Car flying car has received the Certificate of Airworthiness from the Slovak Transport Authority, giving it a push closer to the reality of ma

…

The Air Car flying car has received the Certificate of Airworthiness from the Slovak Transport Authority, giving it a push closer to the reality of mass production.

File photo of AirCar flying car

A car-sized vehicle that can run on roads and fly in the skies as well, seemed a dream few years ago but with various companies globally working on such vehicles, this seems possible now. Meanwhile, Klein Vision’s AirCar flying car that uses a BMW engine, has taken a giant leap closer to getting mass produced.

The AirCar flying car made its maiden flight back in 2020 and completed its first inter-city flight in June last year and now, the vehicle has received the Certificate of Airworthiness from the Slovak Transport Authority, CarScoops reported. To achieve this milestone, the flying car underwent more than 70 hours of testing which included some series of actions and some touch and goes.

With another feather in its hat, which is the new certification, the flying car is getting closer towards the final goal of mass production. “AirCar certification opens the door for mass production of very efficient flying cars. It is official and the final confirmation of our ability to change mid-distance travel forever,” Stefan Klein, leader of the development team and the test pilot told CarScoops.

Klein Vision might currently be the only company this close to real tangible production of a flying car, the publication reported. The company is aiming for the public version of the flying car to have up to 1,000 km or 621 miles of range. It is powered by a 140 hp 1.6-liter four-cylinder BMW engine and has a fixed propeller and a ballistic parachute.

The flying car is capable of racing at a speed of 170 kmph and can fly up to the distance of 1,000 km at an altitude of 8,200 ft. The vehicle also has the ability to make some maneuvers mid-air.

Flying cars have been in discussion for quite some time and these vehicles are being considered as the future medium of city commuting and inter-city transport as the roads are becoming increasingly congested.

इस शेयर का भाव बीते 5 दिनों में 8 फीसदी चढ़ा है, जबकि पिछले एक महीने के हिसाब स करीब 3 फीसदी के फायदे में है. 6 महीने में भाव 1 फीसदी से ज्यादा के नुकसान में है तो एक साल में 33 फीसदी से ज्यादा के फायदे में है.

हालांकि लॉन्ग टर्म में यह शेयर जबरदस्त मल्टीबैगर साबित हुआ है. पिछले 5 साल में इसके भाव में 1 हजार फीसदी की, जबकि 10 साल में 8 हजार फीसदी की तेजी आई है.

ब्रोकरेज फर्म मोतीलाल ओसवाल का मानना है कि यह शेयर अब भी खरीदने लायक है. मोतीलाल ओसवाल ने शेयर को बाई रेटिंग दी है और 1800 रुपये का टारगेट दिया है.

ब्रोकरेज फर्म के अनुसार, निकट भविष्य में कंपनी की डिमांड कम रह सकती है, लेकिन उसके चलते कोई बड़ी परेशानी आएगी, इसकी कम ही आशंका है.

मोतीलाल ओसवाल को चुनाव के बाद इस शेयर की शानदार वापसी की उम्मीद है. उसका कहना है कि चुनाव बाद इंफ्रा पर खर्च बढ़ेगा और डीलर स्टॉक बढ़ाने पर खर्च करने लगेंगे, जिससे इस शेयर को फायदा होगा.

डिस्क्लेमर: यहां मुहैया जानकारी सिर्फ सूचना हेतु दी जा रही है. यहां बताना जरूरी है कि मार्केट में निवेश बाजार जोखिमों के अधीन है. निवेशक के तौर पर पैसा लगाने से पहले हमेशा एक्सपर्ट से सलाह लें. ABPLive.com की तरफ से किसी को भी पैसा लगाने की यहां कभी भी सलाह नहीं दी जाती है.

Personal loans are loans that are not secured by collateral, such as a car or house. This makes them versatile for a variety of purposes, including travel. The following are some factors to consider before taking out a personal loan for travel:

Check how much you need: Creating a comprehensive budget is essential before obtaining a personal loan for travel. Maintaining a 10-15% buffer is crucial for several reasons, including unexpected fees that can arise during travel, such as baggage fees, international transaction fees on credit cards, or resort charges. Additionally, it’s always prudent to plan for the unexpected, such as a lost passport or a minor illness requiring medical care. You might come across the perfect handcrafted souvenir or encounter an unforgettable activity that you’ll want to indulge in.

Interest rates: Personal loans often come with higher interest rates compared to other loan options like home equity loans or credit cards with low introductory APRs. As a result, you may end up paying more in interest over the loan’s duration. A lower APR translates to a reduced overall cost for the loan. Therefore, it’s important to select a lender that offers competitive rates and flexible repayment terms that align with your budget. Ideally, opt for a loan term that enables you to comfortably pay off the loan before your next vacation.

Repayment: You’ll need to make monthly payments on the loan, which will include both the principal amount and interest. Make sure you can comfortably manage these payments along with your other regular expenses.

Once you’ve selected a lender, it’s time to apply for a personal loan. Complete the application form and submit all required documents, including proof of income, identification, and address. The lender will assess your application and credit score to determine your eligibility for the loan.

Utilising a personal loan can be a method to fund your travel, but it’s not the sole option. It’s essential to explore other alternatives that might better suit your circumstances. Explore other ways to fund your trip, like saving in advance, using a travel rewards credit card, or seeking out travel promotions and discounts. Deciding whether to use a personal loan for travel is a personal choice. Carefully consider the advantages and disadvantages to determine if it’s the best option for you.

Frequently Asked Questions (FAQs)

Q. What documents are needed for a personal loan application?

The eligibility requirements and required documentation for a personal loan differ between salaried employees and self-employed professionals. Before applying for a personal loan, it’s recommended to verify your eligibility.

Most financial institutions typically ask for the following documents when applying for a personal loan

For salaried employees

Application: Completed application form with a photograph attached

Proof of identity: A self-attested photocopy of one of the following:

Driving license

Passport

Voter ID

Aadhaar card

PAN card

KYC requirements: You need to provide the necessary KYC documents, including valid proof of identity, residence, and signature.

Income proof: Submit Form 16 or ITR for the past three years and the most recent three months’ salary slips.

Banking details: Provide the latest three months’ salary credit bank statement.

For self-employed individuals

If you are a self-employed professional, you will need to provide the same documents as a salaried employee. However, the banking requirements may vary in this case.

– Banking details: Provide the most recent six months’ business current account statement and the latest three months’ primary savings account statement.

Some loan providers offer a completely digital application process without the need for physical documentation or income proof. This streamlines the personal loan application process and facilitates a fast and efficient disbursal process.

Q. Is it possible to take out a personal loan for medical expenses?

You can utilise a personal loan to handle your medical expenses, particularly if you lack health insurance. It can assist in:

Settling medical bills when you don’t have insurance

Covering medical costs at hospitals not included in your insurance coverage

Financing costly cosmetic procedures

Meeting the expenses of prescription medications

Paying for dental treatments not covered by insurance

Q. Should you take a personal loan to fund travel?

The optimal approach to determining if a personal loan suits you is by evaluating your financial status and travel objectives. If you possess a good credit score and a robust repayment strategy, a personal loan could be a suitable choice. However, if you have reservations about accumulating debt or high interest rates, it’s advisable to investigate alternative financing solutions.

Q. What are the disadvantages of using a personal loan to fund your travels?

The main disadvantages include higher interest rates and increased debt load. Personal loans often come with higher interest rates compared to travel credit cards, and taking out a loan adds to your financial commitments. Additionally, there’s a potential risk of overspending due to the easy availability of cash.

Q. What criteria do lenders typically evaluate when approving a personal loan for travel?

Lenders examine your credit score, income, employment record, and debt-to-income ratio to gauge your repayment capability for the loan.

Milestone Alert!

Livemint tops charts as the fastest growing news website in the world 🌏Click here to know more.

Unlock a world of Benefits! From insightful newsletters to real-time stock tracking, breaking news and a personalized newsfeed – it’s all here, just a click away! Login Now!

Samsung Galaxy Watch 7 series is expected to launch later this year alongside the purported Samsung Galaxy Z Fold 6 and Galaxy Z Flip 6 foldables. The company has yet to confirm the launch of any of the products but there have been several rumours about them over the past few weeks. The Galaxy Watch 7 lineup has been tipped to launch with three possible variants, each with varying connectivity options. Now a report has leaked the battery details of the Galaxy Watch 7 Pro.

A GalaxyClub report spotted the battery details of an upcoming smartwatch on the Safety Korea certification site. The battery with the model number EB-BL705ABY was listed with a rated capacity of 578mAh. This is larger than the rated capacity of the 573mAh rated battery which was used in the Galaxy Watch 5 Pro and marketed as 590mAh.

Therefore, a smartwatch carrying a larger battery than the Galaxy Watch 5 Pro could be the Galaxy Watch 7 Pro. Earlier reports claimed that the Galaxy Watch 7 series is expected to come with three variants – out of which, one is likely a Pro model. Notably, the Galaxy Watch 6 series launched in July 2023 with a base Samsung Galaxy Watch 6 and a Samsung Galaxy Watch 6 Classic.

Samsung’s Galaxy Watch 7 lineup is said to come with Wi-Fi-only and eSIM-supported variants. The former is expected to come with model numbers SM-L300 and SM-L305, while the latter is said to carry model numbers SM-L310 and SM-L315. The rumoured top-of-the-line third variant, expected to be the Galaxy Watch 7 Pro, is likely to carry model numbers SM-L700 and SM-L705. All the model numbers ending with the number five are said to support cellular and eSIM connectivity, while the other models are likely to support only Wi-Fi.

The Galaxy Watch 7 models are also tipped to get 32GB of onboard storage, which is a considerable upgrade over the 16GB on the Galaxy Watch 6 models. The purported smartwatches are expected to run on a new version of Wear OS and One UI Watch and come with an upgraded 3nm chipset which is likely to be 50 percent more power efficient than the current ones.

Affiliate links may be automatically generated – see our ethics statement for details.

By: HT Auto Desk | Updated on: 03 Apr 2024, 07:04 AM

The new norm mandates a single FASTag for one vehicle, barring linking multiple vehicles to a single FASTag or using multiple FASTags for one vehicle.

The One Vehicle, One Fastag’ norm has been implemented from April 1 onwards after NHAI had set a compliance deadline till March 31, 2024 (PTI)

The National Highways Authority of India (NHAI) has implemented the ‘One Vehicle, One FASTag’ norm across the country with effect from April 1, 2024. The new norm mandates a single FASTag for one vehicle, barring linking multiple vehicles to a single FASTag or vice versa. NHAI had set the compliance date for the new rule to April 1, while vehicle owners had until March 31, 2024, to update their FASTag details.

The compliance deadline was extended till the end of March following issues faced by PayTM FASTag users. Under the new norm, multiple FASTags won’t work for a single vehicle. The new regulation is being brought into effect to make the electronic toll collection system more efficient and for seamless movement of vehicles at toll plazas on access-controlled roads.

FASTag has a penetration rate of about 98 per cent and over 8 crore users at present. The new technology uses Radio Frequency Identification (RFID) technology to make toll payments directly from the prepaid or savings account of the vehicle owner to the toll owner.

FASTag has been revolutionary in reducing vehicle pileups at toll plazas and the government has been working on implementing a GPS-based toll collection system as the next step in this direction, ensuring fewer stops.

Canara Bank News Update: अगर आपके या परिवार में किसी सदस्य के अस्पताल में इलाज के दौरान मेडिक्लेम की लिमिट कम पड़ जाए तो आपको अब फिक्र करने की जरूरत नहीं है. बैंक से लोन लेकर आप अस्पताल के बचे हुए बिल का भुगतान कर सकते हैं. सार्वजनिक क्षेत्र की केनरा बैंक ने बुधवार को एक ऐसा लोन स्कीम लॉन्च किया है जिसमें अस्पताल में इलाज के दौरान पैसे कम पड़ जाने के बाद आप बैंक से लोन ले लेकर बिल का भुगतान कर सकते हैं.

इस लोन स्कीम को लॉन्च करते हुए केनरा बैंक ने बताया कि हेल्थकेयर फोकस्ड लोन प्रोडक्ट का नाम केनरा हील (Canara Heal) है. इस लोन प्रोडक्ट का मकसद अस्पताल में इलाज के दौरान पैसे कम पड़ जाने की स्थिति में लोन देकर अस्पताल के बिल का भुगतान करना है. बैंक ने अपने स्टेटमेंट में बताया कि ये लोन अस्पताल में इलाज के लिए भर्ती होने के दौरान सेल्फ या डिपेंडेंट के टीपीए हेल्थकेयर इंश्योरेंस क्लेम के जरिए सेटलमेंट किए जाने के दौरान पैसे कम पड़ जाने पर बैंक लोन देकर बचे हुए रकम का भुगतान करेगी.

केनरा बैंक ने बताया कि अस्पताल के बचे हुए बिल का भुगतान करने के लिए फ्लोटिंग बेसिस पर 11.55 फीसदी के दर पर लोन मिलेगा. जबकि फिक्स्ड रेट के हिसाब से लोन लेने पर 12.30 फीसदी पर बैंक लोन देगी. ये हेल्थकेयर लोन फैसिलिटी उन कस्टमर्स के लिए है जिनके इलाज का खर्च इंश्योरेंस लिमिट से ज्यादा है.

केनरा बैंक ने महिलाओं के लिए केनरा एंजेल नाम से सेविंग अकाउंट प्रोडक्ट को लॉन्च किया है जिसमें कैंसर केयर पॉलिसी जो यूनिक फीचर से लैस है. इसमें प्री-अप्रूव्ड पर्सलन लोन की सुविधा है साथ ही टर्न डिपॉजिट पर ऑनलाइन लोन लेने की भी फैसिलिटी उपलब्ध है. महिलाओं के लिए ये सेविंग अकाउंट पूरी तरह फ्री ऑफ कॉस्ट है साथ ही बैंक की मौजूदा महिला ग्राहक अपने अकाउंट्स में इन फीचर्स को जोड़ने के लिए अकाउंट को अपग्रेड करा सकती हैं.

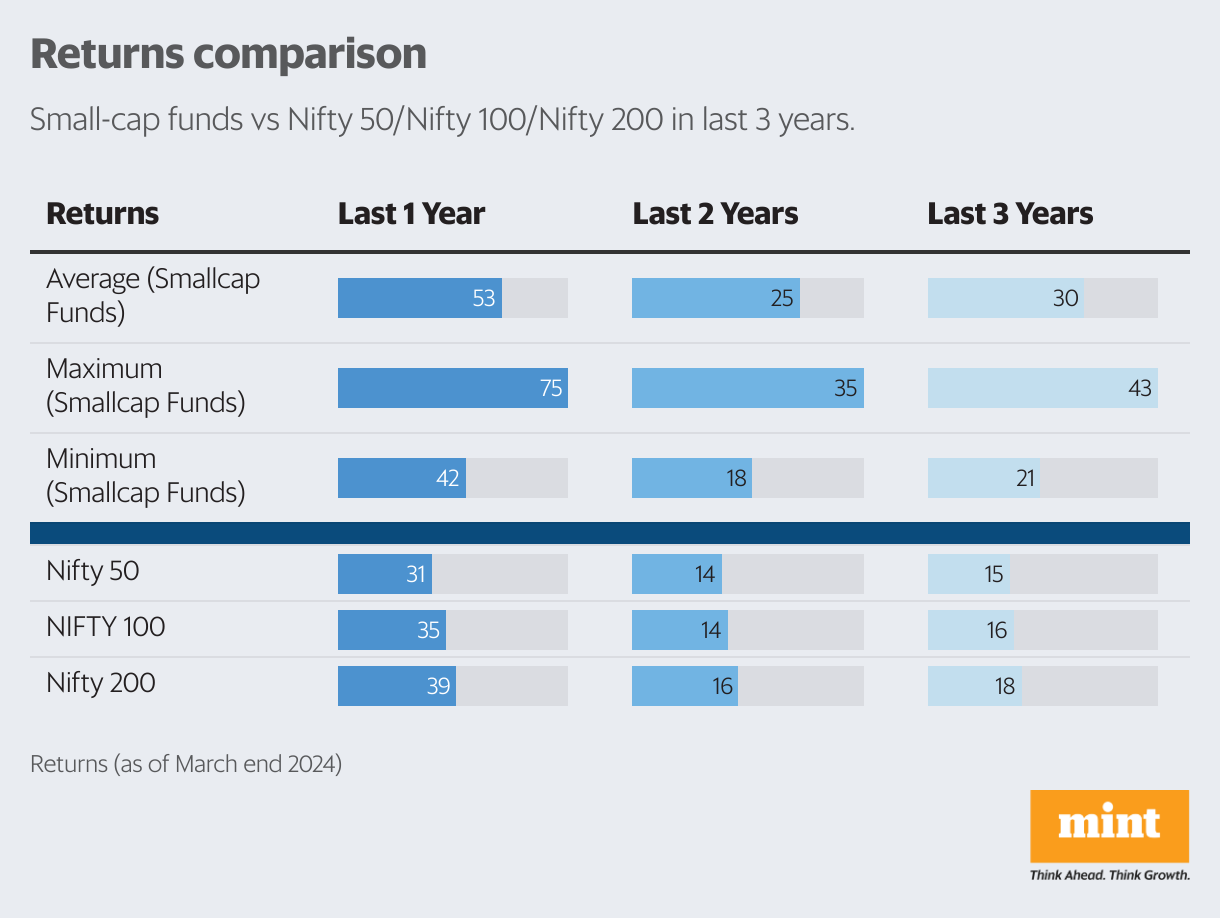

To be fair, staying in small-cap (funds) over the recent past has worked very well for investors. Here is a small aggregate data (of small-cap funds that are at least three years old) that proves this (see graphic).

Irrespective of whether you look at the data of the last one, two or three years data, even the worst small-cap funds have comfortably beaten returns given by large-cap indices like Nifyt50/100 and also large-midcap indices like Nifty200.

And this return profile of the recent past (more specifically the run-up after the pandemic bottom of 2020) has more and more people getting more aggressive with small-caps. New entrants in markets won’t acknowledge (or understand) but mean reversion is still a thing in markets. And given the structurally volatile nature of small-caps, at times, the reversion in this space can be deep and painful. Ask those who have been investing for decades and they will tell you.

This had me thinking. What is the right allocation to have to small-cap funds in a mutual fund (MF) portfolio?

Of course, the answer will vary for different individuals. But still, should one have some guiding guard rails to control the exposure? I think that is required.

Unless you are a professional investor or really have some solid insight about the space, you have no reason to be heavy on small-cap at any time. And this I say for common everyday investors.

In my unsolicited view, if you belong to the balanced or moderately aggressive investors category, then I suggest capping the exposure to small-caps to a maximum of 25-30% of the overall equity exposure.

Many of you may not agree with this view, and more so with recent data to help your case. But let’s remember that even though small-cap funds seem to offer the ‘potential’ for significantly higher future returns than, say, large-caps, they also come with much higher risks compared to large-caps or even mid-caps.

Small-cap funds are a superb choice for taking exposure to small-caps and much better (for common investors) than trying to pick small-cap stocks directly. But don’t be too greedy looking at the recent outperformance and limit yourself to 25-30% in this space. And be willing to remain invested for at least 5-7 years (longer would be better). And what if you have a lower risk appetite and consider yourself to be a conservative sort of investor? In that case, just skip small-cap funds. You don’t need them. The small equity exposure you need is best managed via large-cap funds or flexi-cap funds. That’s it.

I don’t have a crystal ball to tell you whether the ongoing party of small-caps (even after the recent small correction) is over or will still go on. But given what the space has delivered in recent times, it is definitely good to be cautious. If nothing else, I would leave you with one takeaway (that I gave earlier too), do not let your small-cap exposure go beyond 30%. In roaring bull markets, you will be tempted to do so. But it’s good to rebalance and bring it back to saner levels. And if you are still not convinced and still have a small-cap heavy portfolio, I strongly suggest you go and talk to a good investment adviser.

Dev Ashish is a registered investment adviser and founder of Stable Investor

(The views expressed above should not be considered professional investment advice or advertisement or otherwise.)

Samsung launched the Galaxy S24 series running on Snapdragon and in-house Exynos chipsets in January. The South Korean technology conglomerate was tipped last month to fully switch to Exynos SoCs for the entire Galaxy S25 lineup next year. A new report, however, contradicts the claim and says that Samsung will once again opt to split its Galaxy S25 smartphones between Snapdragon and Exynos chipsets. The company will reportedly utilise Qualcomm’s Snapdragon 8 Gen 4 and Exynos 2500 chipsets for its next generation of flagship Galaxy S series smartphones.

According to a report by DigiTimes Asia (via SamMobile), Samsung will stick with its strategy of using both Qualcomm and Exynos chipsets for its Galaxy S series smartphones. The report does not specify which phones in the lineup will run on Snapdragon 8 Gen 4, but we can expect the Qualcomm SoC to feature on the top-of-the-line Galaxy S25 Ultra in all markets. Other phones in the series — likely to be Galaxy S25 and Galaxy S25+ — could feature the Exynos 2500 chipset or Snapdragon 8 Gen 4, depending on the region where they are sold.

The Galaxy S24 Ultra runs on Qualcomm’s Snapdragon 8 Gen 3 globally, while the in-house Exynos 2400 SoC powers the base Galaxy S24 and Galaxy S24+ in markets outside the US, including India.

Last month, a rumour claimed that Samsung may use either an Exynos SoC or a Snapdragon chip, depending on the region, even on the Galaxy Z Fold 6 and Galaxy Z Flip 6 foldables. This would be a departure from Samsung’s usual practice of packing Snapdragon processors in its Galaxy Z Fold and Galaxy Z Flip smartphones.

Samsung is also working on closing the performance gap between Qualcomm and Exynos chipsets. Last week, a tipster claimed that the company’s Exynos 2500 processor outperformed the current Snapdragon 8 Gen 3 SoC in terms of both CPU and GPU performance. The claim, however, was not backed by any performance metrics and benchmark numbers.

While there are no benchmarks available yet, the Exynos 2500 chipset is said to comprise a Cortex-X5 core clocked at 3.2GHz or more, three Cortex-A730 cores at up to 2.5GHz, two more Cortex-A730 cores, and four Cortex-A520 cores with undisclosed clock speeds.

Early in March, the Galaxy S25 series was tipped to run entirely on Samsung’s Exynos chipset. Qualcomm’s Snapdragon 8 Gen 4 chipset, meanwhile, has been confirmed to launch with a custom Oryon CPU at the Snapdragon Summit in October. The chipset is expected to power upcoming flagship Android phones like Samsung Galaxy S25, Xiaomi 15 series, and Asus Zenfone 11.

Affiliate links may be automatically generated – see our ethics statement for details.

By: HT Auto Desk | Updated on: 03 Apr 2024, 07:20 AM

Suzuki Motorcycle India sold 11,33,902 units between March 2023 and April 2024, as against 938,371 units sold during the same period in FY2023, record

…

Suzuki Motorcycle India sold 11,33,902 units between March 2023 and April 2024, as against 938,371 units sold during the same period in FY2023, recording its highest annual sales ever.

Suzuki closed the previous financial year on a high with a 21 per cent jump in year-on-year volumes, while sales in March 2024 increased by 18 per cent

Suzuki Motorcycle India announced its sales for FY2024 and the company registered a 21 per cent growth in the previous financial year. The two-wheeler giant sold 11,33,902 units between March 2023 and April 2024, as against 938,371 units sold during the same period in FY2023, recording its highest annual sales ever.

Out of the nearly 11.34 lakh units sold last fiscal, Suzuki’s domestic sales stood at 921,009 units in FY2024, growing by 26 per cent over 730,756 units sold in FY2023. Exports stood at 212,893 units, growing by 3 per cent when compared to 207,615 units sold in the 2022-23 financial year.

Suzuki’s scooter range continues to dominate its two-wheeler sales, followed by 150 cc and above mass-market motorcycles

Suzuki’s monthly sales in March 2024 remained in the green with a 6.2 per cent growth year-on-year. The company sold 103,669 units last month, as against 97,584 units in March 2023. Domestic sales in March stood at 86,164 units, registering an 18 per cent growth over 73,069 units sold in March 2023. Exports stood at 17,505 units last month, down by 28.59 per cent over 24,515 units shipped overseas in March 2023.

Speaking about the sales, Kenichi Umeda, Managing Director – Suzuki Motorcycle India, said, “We are extremely thankful to all our customers, dealer partners, suppliers and SMIPL team members for their support in achieving the highest ever sales in FY2023-24. SMIPL’s performance in FY2023-24 showcases the immense trust and confidence that customers have shown in Suzuki two-wheelers. As we continue to innovate and expand our offerings, we look forward to further strengthening our position in the Indian two-wheeler market.”

Suzuki’s majority of sales come from its scooter range comprising the Access, Burgman Street and Avenis scooters. The Gixxer 155 and Gixxer 250 series follow, while premium motorcycles including the Hayabusa and Katana bring in a handful of numbers. The Japanese two-wheeler maker recently launched the Suzuki V-Strom 800DE in the country, bringing the middleweight adventure tourer at a competitive price of ₹10.30 lakh (ex-showroom).

Pakistan Bangladesh Economy: पाकिस्तान और बांग्लादेश की जनता पर गरीबी का खतरा मंडरा रहा है. वर्ल्ड बैंक (World Bank) की रिपोर्ट के अनुसार, पाकिस्तान और बांग्लादेश की इकोनॉमी बड़े संकट में है. अगर जल्द हालत नहीं सुधरे तो पाकिस्तान में लगभग एक करोड़ और बांग्लादेश में 10 लाख से ज्यादा लोग गरीबी रेखा के नीचे चले जाएंगे. वर्ल्ड बैंक ने अपनी द्विवार्षिक रिपोर्ट में पाकिस्तान का इकोनॉमिक ग्रोथ रेट सिर्फ 1.8 फीसदी और महंगाई 26 फीसदी रहने की आशंका जताई है. उधर, बांग्लादेश में गरीबी दर बढ़कर 5.1 फीसदी होने का अनुमान लगाया है.

पाकिस्तान में गरीबी दर 40 फीसदी रहने की आशंका

वर्ल्ड बैंक ने अपनी रिपोर्ट में कहा है कि पाकिस्तान के सामने कैश का बड़ा संकट खड़ा हुआ है. यह देश अपने सारे इकोनॉमिक लक्ष्य को हासिल करने में विफल हो सकता है. अंतरराष्ट्रीय मुद्रा कोष (IMF) से मदद मिलने के बावजूद पाकिस्तान की अर्थव्यवस्था में कोई खास सुधार आने की उम्मीद नहीं है. ऐसी आर्थिक परिस्थितियां और महंगाई का बढ़ता दबाव लोगों को गरीबी रेखा के नीचे धकेल सकता है. देश में गरीबी की दर 40 फीसदी के आसपास रहने की आशंका है. फिलहाल लगभग 9.8 करोड़ पाकिस्तानी गरीबी के दलदल में फंसे हुए हैं. अब इस कुचक्र में एक करोड़ लोग और फंस सकते हैं.

कॉस्ट ऑफ लिविंग में हुआ इजाफा, फूड सिक्योरिटी भी मुश्किल

वर्ल्ड बैंक के मुताबिक, पाकिस्तान में कृषि उत्पादन बढ़ने की उम्मीद है. मगर, रिपोर्ट में कहा गया है कि बहुत ज्यादा महंगाई और लगभग सभी सेक्टर्स में वेतन वृद्धि न के बराबर होने के चलते इससे बहुत फायदा होता नहीं दिख रहा. देश में ट्रांसपोर्ट कॉस्ट, स्कूलों की फीस और इलाज का बढ़ता खर्च परिवारों को संकट में डाल रहा है. देश में सरकार द्वारा किए जा रहे प्रयास नाकाफी साबित हो रहे हैं. साथ ही फूड सिक्योरिटी भी मुश्किल में फंसती दिखाई दे रही हैं.

बांग्लादेश में लोगों की कमर तोड़ रही महंगाई

उधर, बांग्लादेश में लगभग 10 लाख लोगों के गरीबी रेखा में पहुंचने की आशंका जताई गई है. वर्ल्ड बैंक ने इनकी दैनिक कमाई 3.65 डॉलर से कम होने का अनुमान जताया है. इनमें से लगभग 5 लाख लोग अत्यधिक गरीबी में फंस सकते हैं. बांग्लादेश में महंगाई दर 9.6 फीसदी रहने का अनुमान है. इसका दबाव झेलना जनता को बहुत भारी पड़ने वाला है.

_1625066791564_1642996658980.jpeg)